Key Components of Financial Independence:

Financial Literacy and Education: Acquiring knowledge about personal finance, investments, debt management, and understanding the impact of financial decisions.

Budgeting and Smart Spending: Creating and adhering to a budget, prioritizing needs over wants, and controlling expenses to save for future goals.

Debt Management and Elimination: Strategically managing and reducing debt, whether it's credit card debt, student loans, or mortgages, to free up resources for investments and savings.

Building Multiple Income Streams: Diversifying income sources through investments, side hustles, rental properties, or passive income streams to increase financial stability.

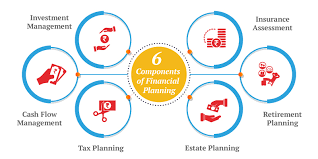

Investment Strategies: Developing a sound investment plan tailored to individual risk tolerance and goals, whether it's through stocks, real estate, retirement accounts, or other investment vehicles.

Emergency Fund and Contingency Planning: Setting aside funds for unexpected expenses or emergencies, ensuring financial stability during unforeseen circumstances.

The Journey to Financial Independence:

Setting Financial Goals: Establishing short-term and long-term financial goals, whether it's early retirement, travel, entrepreneurship, or philanthropy.

Creating a Financial Plan: Developing a comprehensive financial plan outlining income, expenses, savings, investments, and milestones to track progress.

Living Below Means: Practicing frugality, living below one's means, and avoiding lifestyle inflation to save and invest surplus income.

Continuous Learning and Adaptation: Staying informed about changing financial landscapes, adjusting investment strategies, and seeking opportunities for growth.

Strategies for Achieving Financial Independence:

Saving and Investing: Cultivating disciplined saving habits and investing early and consistently to benefit from compound interest and market growth.

Passive Income Generation: Creating sources of passive income through dividends, rental properties, royalties, or online businesses to supplement active income.

Real Estate Investments: Exploring real estate opportunities, such as rental properties or real estate investment trusts (REITs), for potential income streams and asset growth.

Retirement Planning: Contributing to retirement accounts like 401(k)s, IRAs, or pensions to secure financial stability during retirement years.

Entrepreneurship and Side Hustles: Exploring entrepreneurial ventures or side businesses to generate additional income and diversify revenue streams.

Challenges and Strategies:

Market Volatility: Mitigating risks associated with market fluctuations through diversified investments and long-term investment strategies.

Healthcare and Insurance: Planning for healthcare expenses, securing insurance coverage, and considering health savings accounts (HSAs) for future medical needs.

Economic Changes and Inflation: Adapting financial plans to account for inflation, economic shifts, and changes in living costs.

Benefits of Financial Independence:

Freedom to Pursue Passions: Having the liberty to explore interests, hobbies, or career changes without financial constraints.

Reduced Stress and Anxiety: Achieving financial stability can alleviate stress, anxiety, and worries associated with financial insecurity.

Legacy Building and Philanthropy: Having the capacity to leave a legacy, support causes, or engage in philanthropy that aligns with personal values.

Community and Mentorship:

Learning from Others: Seeking guidance from financial experts, mentors, or joining communities that share similar financial goals for support and advice.

Teaching and Sharing Knowledge: Paying it forward by educating others, mentoring, or sharing experiences to help others achieve financial independence.

Financial independence isn't solely about accumulating wealth; it's about creating a life of freedom, security, and the ability to make choices that align with personal values and aspirations. It involves intentional planning, disciplined execution, and a commitment to long-term financial well-being.

Advanced Investment Strategies:

Tax-Efficient Investing: Employing strategies like tax-loss harvesting, maximizing contributions to tax-advantaged accounts, and understanding tax implications on investments.

Portfolio Diversification: Building a well-diversified investment portfolio across various asset classes and geographical regions to mitigate risk and maximize returns.

Asset Allocation and Rebalancing: Regularly reviewing and adjusting asset allocation to maintain a balance between risk and return, aligning with long-term financial goals.

Early Retirement Planning:

FIRE Movement (Financial Independence, Retire Early): Embracing principles of aggressive saving, frugal living, and strategic investments to achieve early retirement goals.

Withdrawal Strategies: Planning withdrawal strategies during retirement to ensure sustainable income while preserving the investment portfolio.

Healthcare and Long-Term Care: Anticipating healthcare costs during retirement, considering insurance options, and planning for long-term care needs.

Entrepreneurship and Passive Income:

Building Businesses: Exploring entrepreneurship opportunities, creating scalable businesses, and leveraging technology for sustainable income streams.

Dividend and Interest Income: Investing in dividend-paying stocks, bonds, peer-to-peer lending, or high-yield savings accounts to generate passive income.

Rental Properties and Real Estate Crowdfunding: Engaging in real estate investments through rental properties or participating in real estate crowdfunding platforms for income generation.

Legacy and Estate Planning:

Estate Protection and Wills: Creating a comprehensive estate plan, including wills, trusts, and power of attorney, to protect assets and ensure wishes are fulfilled.

Charitable Giving and Philanthropy: Incorporating charitable donations or establishing foundations to support causes and leave a lasting impact.

Generational Wealth: Educating future generations about financial responsibility, wealth management, and the importance of values in preserving wealth.

Financial Independence for Specific Life Stages:

Millennials and Gen Z: Addressing student loan debt, focusing on savings, and harnessing technology for financial planning and investment opportunities.

Gen X and Mid-Career Professionals: Balancing retirement savings, career growth, and preparing for potential career transitions or entrepreneurial endeavors.

Seniors and Retirement: Adjusting investment strategies for income preservation, estate planning, and ensuring financial security during retirement years.

Continued Learning and Networking:

Financial Education and Courses: Engaging in advanced financial education, attending seminars, or pursuing certifications to enhance financial knowledge.

Networking and Mentorship: Building relationships with industry experts, seeking mentorship, and joining networks for ongoing guidance and support.

Financial Coaching and Consultation: Seeking professional financial advisors or coaches to optimize financial strategies and address specific financial goals.

The journey to financial independence is dynamic, evolving, and highly personalized. It requires ongoing learning, adaptability, and a proactive approach to financial planning and decision-making, ultimately empowering individuals to achieve greater control over their financial futures.

You must be logged in to post a comment.